Picture this: a customer browses your website, spends ten minutes comparing products, adds an item to the cart, reaches the checkout page and then quietly closes the tab.

No error message. No complaints. No explanation.

This happens millions of times a day across the internet. And while businesses often blame the price, the product or the design, the real culprit is usually something far less visible: perceived risk.

Risk perception in online payments is one of the most underexamined forces in eCommerce psychology. It does not announce itself. It does not leave a paper trail. It operates quietly in the shopper’s mind, a flicker of doubt, a moment of hesitation, a question that goes unanswered and then the sale is gone.

Understanding this hidden anxiety is not just an academic exercise. It is one of the most practical things any online business can do to increase trust, reduce checkout abandonment and convert more visitors into paying customers.

What Is Risk Perception in Online Payments?

Risk perception refers to a consumer’s subjective evaluation of the likelihood and severity of a negative outcome before making a purchase. In the context of online payments, it is the mental calculation a shopper makes, often unconsciously, when about to hand over financial information to a website.

This concept was first studied systematically by Raymond Bauer in 1960, who proposed that all consumer behavior involves risk because any action can produce outcomes that cannot be predicted with certainty. Since then, decades of research have established that perceived risk is a multidimensional construct, meaning it is not just one fear but a cluster of distinct anxieties that all activate simultaneously at the payment stage.

What makes it particularly challenging for online businesses is that perceived risk need not be grounded in reality to be effective. A customer can perceive high risk on a completely secure website. Conversely, objectively risky sites can feel safe to uninformed shoppers. Perception, not fact, drives behavior.

5 Types of Perceived Risk Users Feel at Checkout

Research across consumer psychology identifies six core dimensions of perceived risk that influence online payment behavior. Each represents a different type of anxiety that shoppers bring to the checkout experience.

| Risk Type | What It Means | Impact on Shoppers |

| Financial Risk | Fear of losing money through fraud, failed transactions, or refund issues | Reduces trust and discourages purchases |

| Privacy Risk | Concern about personal data being misused or exposed | Makes users hesitant to share payment information |

| Performance Risk | Doubt that the product or service will meet expectations | Lowers purchase confidence and intent |

| Psychological Risk | Fear of regret, anxiety, or making a poor decision | Creates hesitation and increases cart abandonment |

| Time Risk | Worry about wasting time on slow or complicated checkout processes | Causes frustration and leads users to leave checkout |

1. Financial Risk

The most instinctive fear is losing money. Financial risk perception encompasses the worry that a transaction will result in unauthorized charges, billing errors, undelivered goods, or the inability to get a refund. It is the voice in the back of the shopper’s mind asking, “What if I pay and get nothing?”

This fear is not irrational. Annual global fraud losses on credit and debit cards are projected to reach $48 billion in 2025. About 24% of consumers reported experiencing credit card fraud in the last year, with Gen Z consumers the most affected at 41%. When shoppers arrive at a checkout page, many of them have already been burned, or know someone who has.

2. Privacy Risk

Privacy risk is the fear that sharing personal data, including name, address, card number and email, will result in that information being misused, sold, or exposed in a breach. This goes beyond financial loss into a deeper sense of vulnerability.

The number of individuals impacted by data compromises grew by roughly 1 billion in 2024, reaching 1.35 billion, a figure that reflects how normalized large-scale data exposure has become. For shoppers, every checkout form is a potential entry point for that kind of exposure. Privacy risk perception spikes particularly on unfamiliar websites, where there is no established track record to fall back on.

3. Performance Risk

Performance risk is the doubt that a product or service will actually live up to expectations. Unlike financial risk, which is about losing money, or privacy risk, which is about data, performance risk is about the product itself: “Will this actually do what it claims?”

In eCommerce, this type of risk is heightened by the inability to physically examine a product before buying. Shoppers compensate by looking for reviews, detailed descriptions and return policies. When those signals are absent or unconvincing, performance risk perception increases and purchase intent drops.

4. Psychological Risk

Psychological risk is subtler. It is the fear of making a decision one will regret, of feeling foolish, or of experiencing post-purchase anxiety. Researchers describe it as a potential negative effect on a consumer’s self-esteem or self-perception resulting from a purchase decision.

This type of risk is highest for high-involvement purchases, such as expensive items or items tied to identity and social image. Still, it also surfaces at checkout for any unfamiliar brand.

The moment a shopper senses something is “off” about a website, whether it is a mismatched logo, an unusual redirect, or inconsistent copy, psychological risk activates. Doubt creeps in. And doubt kills conversions.

5. Time Risk

Time risk is the concern that a purchase will waste time through complicated checkout flows, slow page loads, failed transactions that need re-entering, or post-purchase hassles like returns and disputes.

Most of the shoppers will abandon their carts while checking out if they have to re-enter credit card or shipping information and 90% will leave if a site is too slow to load.

These are not just UX problems. They are manifestations of time risk perception. Every extra step, every page load and every unnecessary form field signal to the shopper that their time is not valued.

Why Perceived Risk Is Worse Than Actual Risk

Here is the paradox that every online business needs to understand: perceived risk and actual risk are not the same thing and perceived risk is far more dangerous to conversion rate.

A website can be completely PCI-compliant, running on bank-level encryption, with a spotless fraud record and still lose customers at checkout because the page does not look trustworthy.

Research consistently confirms that consumer decisions are driven by subjective perception (an individual’s personal interpretation of reality, shaped by unique experiences, emotions, beliefs, and senses rather than objective facts), not objective reality (the concept that the universe, facts, and physical objects exist independently of human thoughts, feelings, perceptions, or consciousness).

Consumer trust reduces perceived risk and enhances shopping satisfaction, meaning that the experience of trust is a direct lever on the experience of risk. Build trust and risk perception falls. Fail to signal trustworthiness and it does not matter how secure the backend actually is.

This is why two websites with identical security can have dramatically different conversion rates. One communicates safety. The other does not.

The Checkout Moment: Where Risk Perception Peaks

Risk perception is not evenly distributed across the customer journey. It builds gradually, present during product browsing, growing during the consideration phase and reaching its peak at the exact moment of payment.

The global shopping cart abandonment rate sits at over 70%. And while abandoned carts have many causes, security and trust concerns are a consistent contributor. A lack of trust in credit card security accounts for 18% of cart abandonments, according to research tracking the most common checkout exit reasons.

Several specific triggers cause this spike in perceived risk at checkout.

| Checkout Risk Trigger | What It Means | Impact on Conversion |

| Unfamiliar Payment Interfaces | Redirects or payment pages that look inconsistent with the website | Creates distrust and increases checkout abandonment |

| Absence of Security Signals | Missing SSL badges, payment logos, or trust indicators | Makes shoppers question payment safety |

| Forced Account Creation | Requiring users to create an account before checkout | Adds friction, time risk and privacy concerns |

| Unfamiliar Payment Options | Preferred payment methods are unavailable | Reduces confidence and increases hesitation |

| Lack of Social Proof | No reviews, testimonials, or customer activity visible | Weakens trust and lowers purchase intent |

The Psychology Behind the Hesitation

Understanding why perceived risk causes checkout abandonment requires a brief look at how the brain processes financial decisions under uncertainty.

When shoppers reach the checkout stage, they are not only evaluating the value of the product. They are also weighing the potential consequences of something going wrong. This is where several psychological principles come into play:

- Loss aversion: Research in behavioral economics shows that losses feel significantly more painful than gains feel rewarding. At checkout, the fear of losing money, exposing personal information, or facing fraud often outweighs the excitement of making a purchase.

- The endowment effect: Once users add a product to their cart, they begin to feel a sense of ownership over it. However, completing the purchase introduces a larger perceived risk. If something goes wrong after payment, the emotional loss feels greater than simply abandoning the cart.

- Uncertainty amplification: When people do not have enough information to judge a situation confidently, they tend to overestimate risk. A checkout page without clear security signals, refund information, or transparent next steps increases uncertainty and makes abandonment more likely.

Together, these psychological triggers push users toward the safest perceived option: leaving without completing the purchase.

What Reduces Perceived Risk: The Trust Architecture

If perceived risk is the problem, trust is the solution. And trust, in the context of online payments, is built through what researchers call risk-reduction strategies, which are specific signals and design elements that lower a shopper’s subjective sense of vulnerability.

1. Recognized Payment Methods

Perhaps the single most effective risk-reduction tool is the presence of familiar payment logos. When a shopper sees Stripe, PayPal, Visa, or Mastercard at checkout, they are not just seeing a payment option. They are seeing a trusted intermediary. The brand equity of those logos transfers to the transaction.

Factors that build trust at the payments page include the customer being able to choose their preferred payment method, along with logos of recognized payment methods such as Visa and Mastercard.

The psychological mechanism is straightforward: if a shopper’s bank or favorite payment provider is involved, there are known dispute resolution processes in place. Risk feels managed.

2. Security Badges And Trust Signals

Visible security indicators directly reduce security risk perception. SSL padlock icons, “Secure Checkout” labels and recognizable trust seals all communicate that the payment infrastructure has been independently verified.

Most consumers say they buy more often when they see trust signals. The placement matters as much as the presence. Security badges should sit right next to payment fields and privacy assurances near form fields boost completion rates.

3. Transparent Pricing

Surprise costs are a primary driver of checkout abandonment and they activate financial risk perception directly. When the total at checkout is higher than expected, the shopper’s financial risk calculation recalibrates upward and the purchase suddenly feels riskier than it did on the product page.

Showing all-inclusive pricing early in the journey, including shipping, taxes and fees, removes the shock and keeps the shopper’s mental commitment intact.

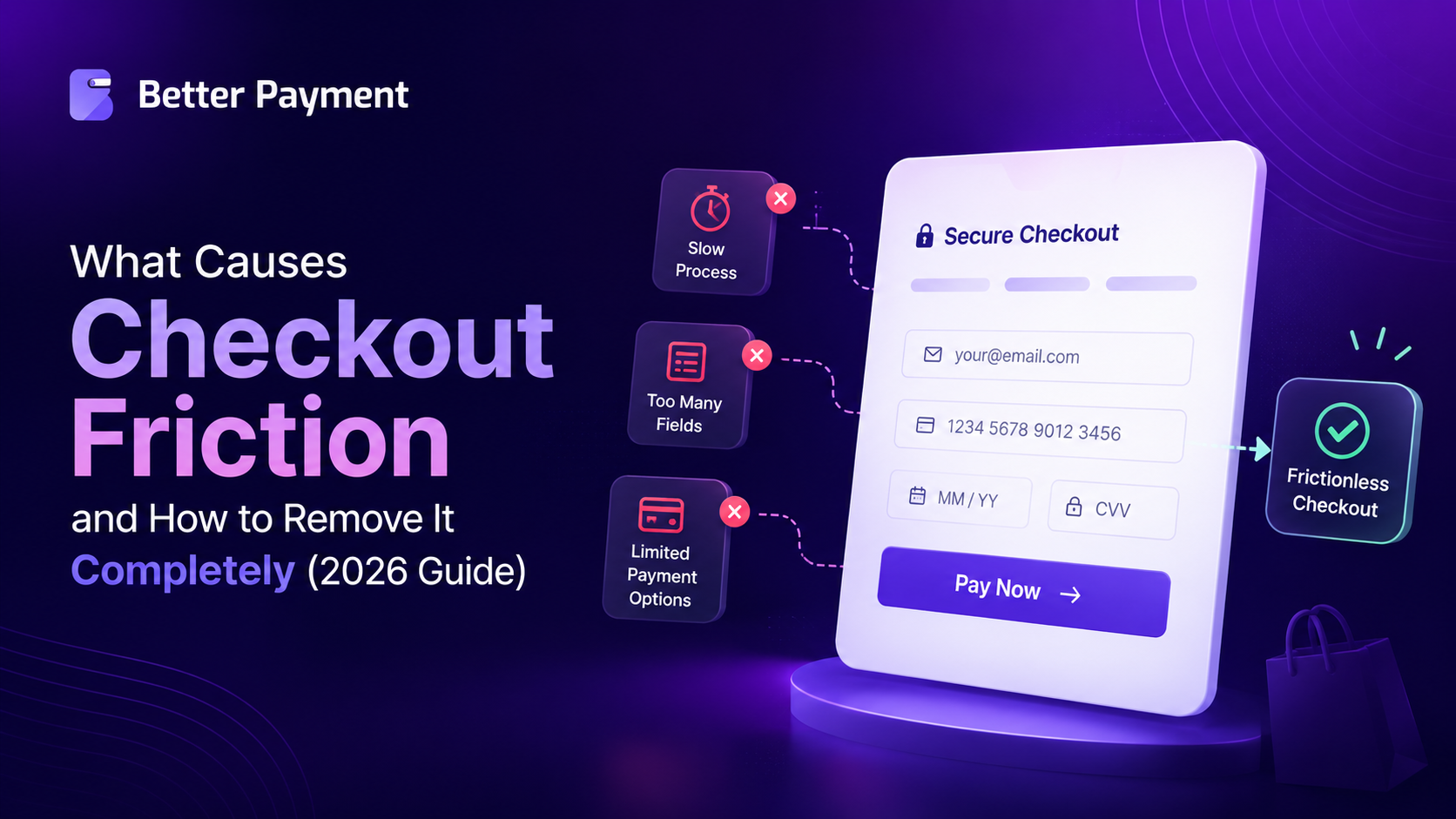

4. Simplified Checkout Flows

Every additional step in a checkout process is a new decision point. And every decision point is an opportunity for risk perception to reassert itself. Research is clear that shorter, simpler checkout flows reduce time risk and psychological risk simultaneously.

19% of online shoppers abandon their purchases due to overly complicated checkout processes, and among consumers aged 30 to 44, this figure jumps to 38%. One-page or minimal-step checkouts remove friction and keep shoppers in a forward momentum that discourages second-guessing.

5. Social Proof

Reviews, testimonials and customer counts serve as powerful risk reducers because they answer the shopper’s implicit question: “Have other people done this and been okay?” Social proof transforms a novel, uncertain transaction into a familiar, validated one.

A product with just 5 reviews has a purchase likelihood 270% higher than a product with no reviews at all. Even a small amount of visible social proof meaningfully shifts risk perception.

6. Guest Checkout Options

Forcing account creation before payment is one of the most reliable ways to spike privacy risk and time risk simultaneously. Offering guest checkout, where customers can pay without registering, removes both barriers in a single design decision.

How Better Payment Addresses Risk Perception by Design

This is where the architecture of a payment solution matters as much as marketing.

Better Payment, the one-click WordPress payment plugin for Elementor and Gutenberg, was built with the friction of the payment moment in mind. It integrates directly with Stripe, PayPal and Paystack; three of the most globally recognized and trusted payment gateways. With this, the solution brings their brand credibility and fraud protection infrastructure directly to the checkout page.

When a customer sees a Stripe, PayPal and Paystack interface, they are not encountering an unknown entity. They are transacting through a system they have likely used dozens of times before. That familiarity collapses perceived risk at the exact moment it matters most.

Beyond the gateway integrations, Better Payment reduces risk perception through several practical design choices.

i. Minimal, clean payment forms. With Elementor and Gutenberg compatibility, Better Payment lets you build streamlined payment forms that collect only what is necessary. There are no bloated multi-step flows that signal complexity and amplify time risk. The cleaner the form, the lower the friction.

ii. Instant confirmation emails. After every transaction, Better Payment automatically sends notification emails to both the customer and the admin. This directly addresses psychological risk, the post-payment anxiety of “Did that go through?”, by providing immediate confirmation that the transaction is complete and recorded.

iii. Payment receipts. Professional, automatically generated receipts give customers a paper trail that reduces financial risk perception. Knowing there is documentation of the transaction is a meaningful trust signal.

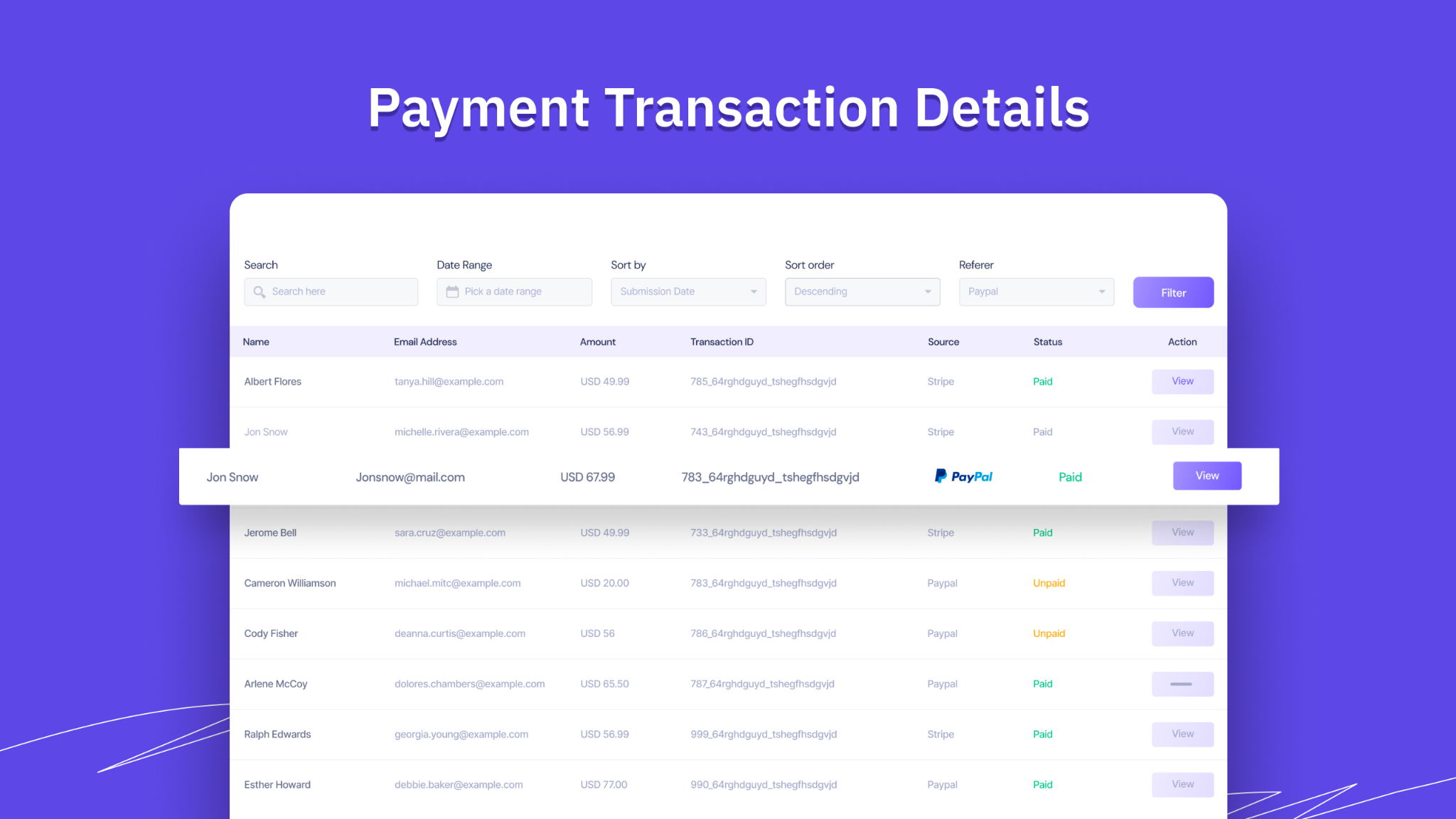

iv. Full transaction history in the WordPress dashboard. Store owners can view all payment records in real time, enabling fast responses to any customer concern, which, when communicated through a clear refund and support policy, further reduces perceived risk for future shoppers.

v. No bloated redirect chains. Unlike payment setups that push customers through multiple unfamiliar third-party pages, Better Payment’s clean integration keeps the payment experience close to the branded environment, reducing the redirect anxiety that contributes to security risk perception.

For WordPress site owners, whether collecting donations, managing membership fees, or running a fundraising campaign, Better Payment provides the trust infrastructure that turns risk-averse browsers into confident buyers.

Practical Steps to Reduce Payment Risk Perception on Your Website

Whether you are just starting or refining an existing checkout experience, here are the highest-leverage changes you can make to address the six dimensions of perceived risk.

👉 Address financial risk: Display your refund and returns policy prominently near the payment button. Use recognizable payment gateways. Show an itemized order summary before the final confirm step.

👉 Address privacy risk: Include a brief, plain-language statement about how payment data is handled, for example, “We never store your card details.” Link to your privacy policy. Use HTTPS everywhere, not just at checkout.

👉 Address performance risk: Add product reviews and ratings close to where purchasing decisions are made. Use specific, detailed product descriptions. Offer a guarantee wherever possible.

👉 Address psychological risk: Keep your brand design consistent through to the payment page. Avoid sudden visual changes, unfamiliar logos, or redirects to pages that look different from the rest of your site.

👉 Address time risk: Reduce form fields to the minimum required. Enable autofill. Show progress if using multi-step checkout. Make error messages helpful and specific.

👉 Address security risk: Display SSL indicators and security badges at the checkout stage. Use payment providers with built-in fraud detection. Consider adding a visible statement that the checkout is encrypted.

The Bottom Line: Trust Is a Conversion Strategy

Risk perception in online payments is invisible, but its impact on revenue is very real.

Every time a shopper abandons a checkout without explanation, there is a good chance it was not the price, the product, or even the design that stopped them. It was a moment of doubt that the experience did not resolve quickly enough. A gap between what they needed to feel safe and what the page communicated.

The good news is that perceived risk is addressable. It responds to design choices, trust signals, payment infrastructure and the language used at the moment of transaction. Businesses that take this seriously, that build their payment experience around the psychology of trust, consistently outperform those that treat checkout as an afterthought.

For WordPress-powered websites, the foundation of that trust starts with the payment tool you choose. A plugin like Better Payment does not just process payments. It positions every transaction as a low-risk, high-confidence interaction, which is exactly what customers need to feel before they click “pay.”

Subscribe to our blog for more payment-related solutions and join our Facebook community to connect with like-minded professionals.